Save Up To 30% On

Get your car insurance within minutes

Enter your car registration details

Don't know your car number? Click here

Brand new car? Click here

11.5 Lakh+

Happy Smiles

930+

Companies Insured

250+

Insurance Products

5.5 Lakh+

Claim Settlements

Car Insurance

Car insurance is a contract between a driver and an insurance company that offers financial protection against accidents, theft, and damage to the vehicle. It typically includes liability coverage for injuries or damage you cause to others, as well as coverage for your own vehicle, such as collision and comprehensive insurance. Additionally, policies may provide personal injury protection for medical expenses and uninsured/underinsured motorist coverage in case you're in an accident with someone lacking sufficient insurance. Having car insurance is often a legal requirement and helps safeguard you financially in unexpected situations.

What is Car Insurance?

Car insurance, also known as motor or four-wheeler insurance, is an agreement between a car owner and an insurance provider that offers financial protection against damage or loss from accidents and natural disasters. It’s essential for covering potential repair costs, as accidents can happen even to careful drivers.

There are three main types of car insurance: Third-Party Car Insurance, Standalone Own-Damage (OD) Insurance, and Comprehensive Car Insurance. Third-party insurance covers only damage to others' property or injuries in accidents where you're at fault. Standalone Own-Damage insurance covers damage to your own vehicle due to accidents, theft, or natural disasters but doesn’t include third-party liability. Comprehensive insurance combines both, offering full protection for your own car, third-party damages, and personal injury, making it the most extensive and costly option..

Types Of Car Insurance

Third Party Car Insurance

In India, third-party car insurance is a legal requirement for driving a car. This coverage ensures that the insurance company compensates for injuries, disabilities (both temporary and permanent), or fatalities suffered by third parties in accidents involving the insured vehicle. It specifically covers damages caused to other people, their property, and vehicles, but does not provide protection for the policyholder's own vehicle or injuries sustained by the driver or passengers.

Comprehensive Car Insurance

This insurance policy is highly favored by car owners because it offers financial protection for both damages to their own vehicle and any harm caused to third parties. As its name implies, it provides extensive coverage, including protection against damages from natural disasters, man-made incidents, self-ignition, lightning, explosions, fires, and theft.

This comprehensive approach ensures that car owners have robust support in various situations. Comprehensive policies may also include personal accident cover for the driver and passengers, roadside assistance, and other add-ons, making it a more expensive but well-rounded option for car owners seeking extensive protection.

Own Damage Car Insurance

In September 2019, the Insurance Regulatory and Development Authority of India (IRDAI) introduced the Standalone Own-Damage (OD) Car Insurance policy. This plan is designed to provide coverage exclusively for damages to the insured vehicle due to road accidents, natural or man-made disasters, fires, explosions, theft, or other similar incidents. It is an ideal option for those who already have third-party insurance but want additional protection for their own vehicle without opting for a comprehensive policy.

Third-Party VS Own Damage Vs Comprehensive Bike Insurance:

| Point of Difference | Third-Party Insurance | Own-Damage Insurance | Comprehensive Insurance |

|---|---|---|---|

| Definition | Covers damages caused to third parties in an accident caused by the insured vehicle. | Covers damages to the insured vehicle only due to accidents, theft, fire, or natural disasters. | Combines third-party liability and own-damage coverage for the insured vehicle. |

| Coverage |

Third-party property damage Third-party injury or death |

Damage to own vehicle from accidents, theft, fire, or natural disasters |

Third-party property damage Third-party injury or death Damage to own vehicle Theft, fire, vandalism, natural disasters |

| Legal Requirement | Yes, mandatory by law in many countries (e.g., India). | Not mandatory, but recommended if you want protection for your own vehicle. | Not mandatory, but highly recommended for full coverage. |

| Cost | The most affordable option. | Moderate cost, as it covers only the insured vehicle. | The most expensive option, due to extensive coverage. |

| Exclusions |

Damage to the insured vehicle Injuries to the driver or passengers |

Third-party damages Personal injuries or death of driver/passengers |

Damage caused by driving under the influence of alcohol or drugs Damage due to driver negligence (e.g., driving without a license) |

| Add-ons | Generally, no add-ons available. | Some policies may offer add-ons like roadside assistance, engine protection, etc. | Wide range of add-ons available, including roadside assistance, zero depreciation, engine protection, etc. |

Who should buy Car Insurance Policy?

Anyone who owns or operates a vehicle should consider buying car insurance. This includes car owners, especially those with new, leased, or high-value vehicles, as well as new drivers and families with teen drivers. Having car insurance provides essential financial protection and ensures compliance with legal requirements, making it a crucial investment for anyone who drives regularly

What Is Covered Under Car Insurance Policy?

- Third Party Death: Compensation will be provided if an accident involving your vehicle results in the death of a third party.

- Road Accidents: Your vehicle will be covered for any damages sustained in accidents or collisions.

- Natural Calamities: Your car will be protected against damages caused by natural disasters such as earthquakes, floods, and cyclones.

- Man-made Disasters: Coverage includes damages to your vehicle from man-made disasters, including riots, strikes, terrorism, and vandalism.

- Damage During Transit: Your car will be insured for damages occurring during transit by road, rail, inland waterways, or lift.

- Fire/Explosion: Damages to your vehicle resulting from fire or explosions will be covered.

- Theft of Your Car: Loss of your vehicle due to theft or burglary is included in your coverage.

What Is Not Covered Under Car Insurance Policy?

- Drunk Driving: Claims for incidents where the insured was driving while under the influence of alcohol will not be accepted.

- Driving Without a Valid Driver’s License: Coverage is not provided if the insured was operating the vehicle without a valid driver’s license.

- Wear and Tear/Depreciation: Typically, depreciation costs related to the vehicle are not covered.

- Consumables: Coverage does not extend to consumables such as engine oil, brake fluid, air conditioning refrigerant, radiator coolant, nuts, bolts, screws, washers, grease, and similar items.

- Mechanical/Electrical Breakdown: There is no coverage for mechanical or electrical failures.

- Driving Under the Influence of Drugs: Claims are not covered if the insured was driving while under the influence of drugs.

- Damage in War/Nuclear Attack: No coverage is available for damages resulting from war or nuclear incidents.

- Damage to Tyres/Tubes Except in Accidents: Generally, damages to tyres and tubes, except in the event of an accident, are excluded from coverage.

- Damage Incurred Outside Covered Geographical Boundaries: Coverage does not apply to damages that occur outside the specified geographical limits.

How to Choose Car Insurance Policy Online?

With three main types of four-wheeler insurance available, it's essential to evaluate your insurance requirements and choose the appropriate policy type. Opt for third-party coverage to meet legal obligations, or select a comprehensive plan for full protection of your vehicle.

The cost of coverage varies based on factors such as Insured Declared Value (IDV), model, fuel type, and age, resulting in different premiums across insurers. It’s important to compare four-wheeler insurance premiums to ensure you choose a plan that fits your budget. Start by reviewing various premiums before making your final choice.

The Insured Declared Value (IDV) represents the current market value of your vehicle. As your car experiences wear and tear, its value diminishes. The IDV is the maximum amount your insurance company will pay in the event of total loss or theft. Remember, the insurance premium is directly linked to the IDV; a higher IDV means a higher premium.

Enhance your policy with various add-ons like zero depreciation cover, no claim bonus, key loss cover, and engine protection. Including these additional options can significantly increase the benefits of your insurance plan. Once you've chosen the right four-wheeler policy, you'll gain comprehensive protection for your car.

Cashless garages simplify the claims process, allowing policyholders to settle claims without upfront payments. Choosing an insurer with a wide network of cashless garages makes repairs easier and more convenient. Always opt for a four-wheeler insurance plan from a company that partners with numerous cashless garages.

The Claim Settlement Ratio (CSR) indicates how effectively an insurance company processes claims. This ratio reflects the percentage of claims settled within a year. Look for an insurer with a straightforward and prompt claims process, and prioritize companies with a high CSR when making your decision.

In addition to the CSR, consider the services provided by your chosen four-wheeler insurance company. Check if they offer fast claim settlements, 24/7 customer support, and other essential services. Select a company known for its responsive and hassle-free customer service.

Make it a priority to compare different car insurance policies online. This process simplifies the selection of a plan that meets your budget and requirements. Assess the coverage options available under various four-wheeler insurance plans to make an informed choice about your insurance.

Car Insurance Add-ons

Zero Depreciation

Zero depreciation cover is an add-on for comprehensive car insurance that lets policyholders claim the full cost of replacing damaged car parts without factoring in depreciation. This means you receive the entire replacement cost rather than a reduced payout based on market value, making it especially valuable for new or high-value vehicles.

This coverage ensures you won’t face financial loss due to depreciation and provides peace of mind by allowing you to restore your vehicle to its pre-accident condition without extra expenses.

24x7 Roadside Assistance

Roadside assistance provides support for vehicle breakdowns while on the road. This service typically includes help with issues such as flat tires, dead batteries, fuel delivery, and locksmith services if you lock your keys inside the car. When you encounter a breakdown, you can contact your insurance provider or roadside assistance service, and they will dispatch a technician to your location to resolve the issue.

This service offers peace of mind, ensuring that you’re not left stranded and can quickly get back on the road, making your driving experience safer and more convenient.

Engine Protection Cover

Engine protection coverage is an add-on feature in car insurance that specifically addresses damages to your vehicle's engine. This coverage typically safeguards against issues like hydrostatic damage (caused by water entering the engine), engine failure due to mechanical faults, and damage from accidents. Without this protection, standard policies may not cover the expensive repairs or replacements that engine issues can incur, which can be a significant financial burden.

By opting for engine protection, you ensure that you have comprehensive coverage against various risks that could compromise your engine’s performance and longevity, allowing you to drive with confidence knowing you’re protected from costly repairs.

NCB Protector

A no-claim bonus (NCB) protection feature in car insurance allows policyholders to maintain their accumulated no-claim bonus even after filing a claim. Typically, insurers reward drivers with a discount on their premium for each claim-free year. However, if you make a claim, you risk losing this bonus, which can lead to higher premiums in the future.

With NCB protection, you can file a claim without losing your bonus, ensuring that your premium remains lower in subsequent policy renewals. This feature is especially beneficial for those who might experience minor accidents or damages but want to keep their cost-saving benefits intact.

Key & Lock Replacement

Key loss cover is an add-on feature in car insurance that provides financial protection for the replacement of lost or stolen vehicle keys and locks. If you lose your car keys or they are stolen, this coverage typically includes costs associated with key replacement, reprogramming of electronic keys, and even the installation of new locks if necessary. This service can be particularly valuable, as replacing lost keys can be costly and time-consuming, especially for modern vehicles with advanced locking systems.

Consumables

Consumables are essential items needed for vehicle repairs, such as engine oil, brake fluid, and small parts like nuts and bolts. These costs are typically not covered under the basic own damage section of standard car insurance policies, leaving policyholders to pay out of pocket for repairs. To address this, some insurers offer add-ons that include consumables coverage, providing financial protection against these necessary expenses.

Daily Allowance

Compensation for daily expenses during vehicle repair is typically provided through a specific add-on or feature in car insurance known as "daily allowance" or "loss of use" coverage. This benefit offers financial support for alternative transportation costs incurred while your vehicle is being repaired due to an accident or damage.

Invoice Price

Invoice cover, or "return to invoice" coverage, is an add-on in car insurance that compensates you for the original purchase price of your vehicle in case of total loss or theft, rather than its depreciated value. This feature is especially beneficial for new car owners, protecting against rapid depreciation.

Tyre Protector

Tyre coverage is an add-on in car insurance that covers repairs or replacements for damaged tyres due to punctures, cuts, or blowouts. Standard policies often exclude tyre damage, leaving you to pay out of pocket. This coverage is especially valuable for drivers in poor road conditions, providing financial protection against unexpected repair costs and enhancing your vehicle’s performance and safety.

Loss of Personal Belongings

Coverage for personal items in your vehicle is an add-on in car insurance that protects against theft or damage to belongings like bags and electronics. Standard policies typically don’t cover these items, leaving you financially vulnerable. With this coverage, you can claim compensation for lost or damaged items up to a specified limit, providing peace of mind for those who carry valuable belongings in their cars.

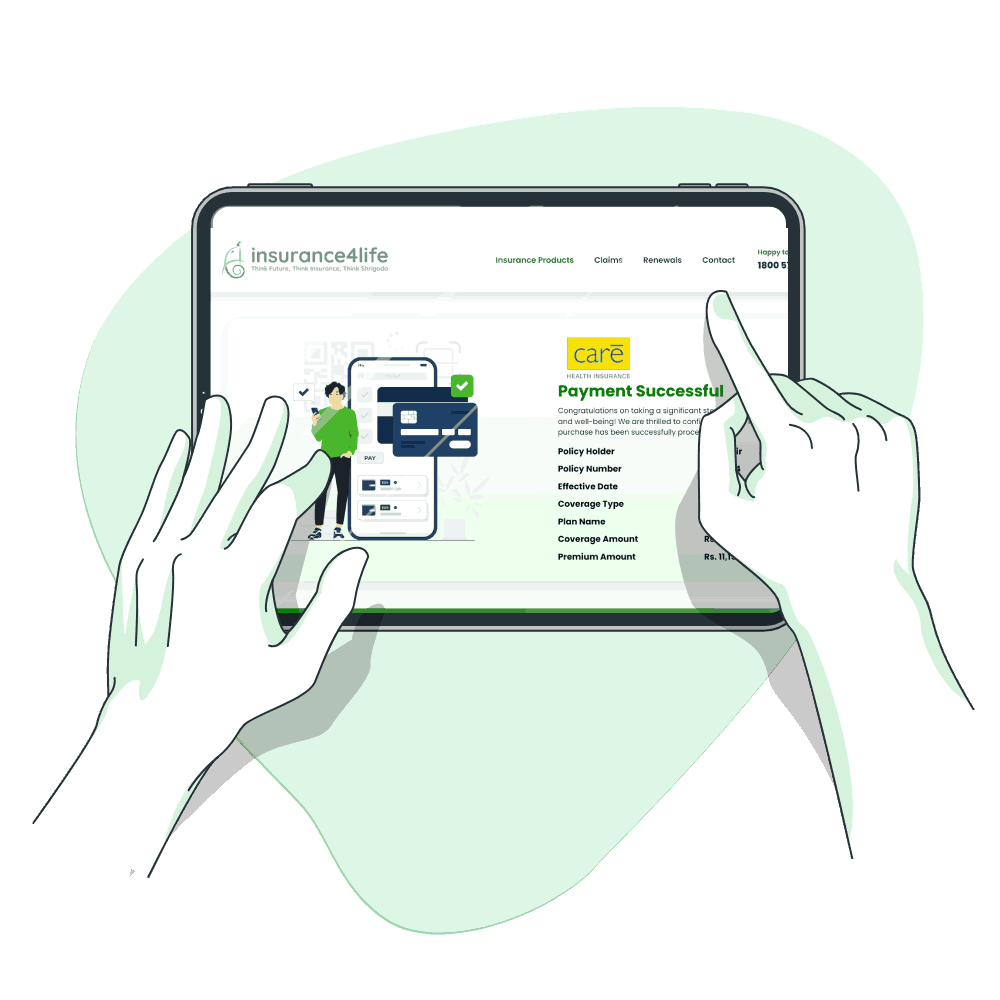

How To Buy Online Policy !

Get Quotes

Share your basic details like number of family members, their age and location

Choose plan

Select the ideal plan based on your needs and budget

Details Verified

Verification completed through secure online CKYC API

Payment Successful

Pay premium online & get your policy copy delivered instantly to your email inbox

FAQs About Car Insurance

Car insurance is a contract between an insurance provider and a car owner, offering financial protection against damages from unexpected events. There are three main types: third-party, standalone own-damage, and comprehensive insurance. The online renewal process allows for immediate issuance of an e-Policy.

Owning four-wheeler insurance offers several advantages. It fulfils the legal requirement for at least third-party coverage and protects you from financial liabilities resulting from accidents or damage to your vehicle.

Choose a reputable insurance provider by evaluating their claim settlement time and ratio. Look for added features such as a network of garages, cashless claims, and convenient online payment and claim options. Conduct a comparative analysis to identify the best insurance provider for your needs.

Comprehensive car insurance provides coverage for a range of incidents, including damage to your vehicle and others. In contrast, third-party car insurance focuses on legal liabilities resulting from accidents caused by the insured driver. Additionally, usage-based motor insurance allows drivers to pay premiums based on the actual mileage they drive.

Your car insurance policy will cover you for a single year. The start and end date of your policy will be clearly marked on your policy documents, so don’t worry. And hey, once you buy a policy, we will send you a renewal reminder in advance so you don’t forget to renew it for the next year.