Group Term Life Insurance

We protect what you love

Fill the following details and compare plans

11.5 Lakh+

Happy Smiles

930+

Companies Insured

250+

Insurance Products

5.5 Lakh+

Claim Settlements

About Group Term Life

Group Term Life Insurance (GTLI) is a type of life insurance provided through an employer or an organization, such as a professional association. Often referred to as "group" or "employer-paid" insurance, the coverage is typically funded by the employer as part of the employee benefits package. GTLI offers basic life insurance protection for employees, with premiums usually covered by the employer, making it an affordable option for many workers. In this article, we’ll explore how GTLI works and help you determine if it’s the right coverage for you.

What Is Group Term Life Insurance?

Group Term Life Insurance (GTLI) is a type of temporary life insurance that provides coverage for multiple individuals under a single contract. Typically offered through an employer, the employer holds the policy and extends coverage to employees as part of a benefits package. Many employers provide a basic level of coverage at no cost, with options for employees to purchase additional coverage for themselves, their spouses, and children. GTLI is also available through various associations and professional organizations.

One of the main benefits of GTLI is its affordability, making it an attractive option for employees compared to individual life insurance policies, resulting in high participation rates.

Advantages of Group Term Life Insurance

No Medical Exams

Most group term life insurance policies do not require a medical exam, making it easier for employees to qualify.

Employer Contribution

In many cases, the employer covers part or all of the premiums, providing a valuable benefit to employees.

Guaranteed Acceptance

Group term life insurance typically guarantees acceptance, so employees cannot be denied coverage due to health conditions.

Cost-Effective

It is generally more affordable than individual life insurance policies, offering significant savings for employees.

Disadvantages of Group Term Life Insurance

No Cash Value

Group term life policies do not build cash value, meaning you cannot borrow against them or receive any return on your premiums.

Loss of Coverage

Coverage may be lost if you leave your employer or the group offering the insurance, potentially leaving you without protection.

Limited Customization

These policies typically offer fewer customization options, making it difficult to tailor coverage to your specific needs.

Limited Coverage

Group term life insurance usually provides lower coverage amounts compared to individual life policies, which may not fully meet your financial needs.

Who should get Group Term Life Insurance?

Group Term Life Insurance is an affordable and valuable option for both employees and employers. It is especially beneficial for employees who may struggle to afford individual life insurance coverage on their own or those who do not have access to it through other means.

Small to medium-sized businesses and organizations can also benefit by offering group coverage as part of their employee benefits package, providing essential life insurance to their workforce without the high costs associated with individual policies. Additionally, employees who need basic life insurance coverage, without the complexity or expense of tailored individual policies, will find group term life insurance to be an accessible and cost-effective option.

How Does Group Term Life Insurance Work?

The employer or organization purchases a policy to cover a group of individuals, such as employees or association members.

The coverage amount is typically determined by the employer, often based on a multiple of the employee's salary or a fixed amount.

Employers usually cover the premiums, though some employees may contribute through payroll deductions.

A key benefit is that group term life insurance generally does not require individual medical assessments or underwriting.

Upon the death of an insured employee, the insurance company pays a lump sum death benefit to the beneficiary, typically tax-free.

Coverage is usually renewed annually, but it ends if the employee leaves the company or retires, depending on the policy terms.

Types of Group Term Life Insurance?

Employer-Sponsored Group Term Life Insurance

Basic Group Term Life Insurance

This coverage is provided by employers as a standard employee benefit. The employer pays the premiums, and the coverage amount is typically a multiple of the employee's salary.

Supplemental Group Term Life Insurance

Employees can purchase additional coverage beyond the basic policy. The employee is responsible for paying the premiums for this extra coverage.

Types of Group Term Life Insurance?

Non-Employer Sponsored Group Term Life Insurance

Association Group Term Life Insurance

Offered through associations or organizations, this type of coverage allows members to purchase life insurance at a discounted rate.

Affinity Group Term Life Insurance

Similar to association coverage, but typically available to members of specific affinity groups, such as credit unions or alumni associations.

Credit Life Insurance

Provided by lenders to borrowers, this policy pays off the outstanding debt if the borrower passes away before the loan is repaid.

Wholesale Group Term Life Insurance

Offered to large groups, such as corporations or labor unions, at a discounted rate. The group then distributes the coverage to its members.

What Is Covered under Home Insurance?

- Natural Disasters: Storms, cyclones, typhoons, hurricanes, tornadoes, floods, inundation, and earthquakes.

- Water Damage: Bursting or overflowing of water tanks, equipment, and pipes.

- Impact Damage: Damage caused by vehicles or animals directly contacting the property.

- Civil Disturbance: Losses from riot, vandalism, or terrorism.

- Fire and Explosions: Damage caused by fire, explosions, or implosion.

- Theft or Attempted Theft: Losses from theft or any attempted theft.

- Robbery & Dacoity: Loss or damage resulting from robbery or dacoity (violent theft).

- Alternate Accommodation: If your home becomes uninhabitable due to an insured event, our policy provides coverage for temporary accommodation, ensuring you have a comfortable place to stay until your home is livable again.

- Accidental Damage: Our insurance plan protects expensive fittings and fixtures from accidental damage, ensuring that both homeowners and tenants can safeguard their valuable belongings.

What Is Not Covered under Home Insurance?

- War-related events: This includes damage caused by invasion, military actions, or any conflict-related activities such as hostilities or war-like operations.

- Damage from hazardous materials: This includes loss or damage resulting from radioactive substances, toxic chemicals, or explosives.

- Criminal acts with intent: Losses arising from intentional criminal actions, such as arson, theft, vandalism, or other illegal activities, are not covered.

- Wilful negligence or misconduct: Insurance will not cover damage caused by deliberate actions or gross carelessness, such as intentional harm to property or reckless behaviour that leads to loss or damage.

Add-Ons under Home Insurance:

Choose from a variety of add-on coverages to enhance your policy's protection.

Loan Payment Protection

In the unfortunate event of an accident that leads to the insured's death or disability, this add-on provides coverage for any outstanding loan payments.

Fixed Glass & Sanitary Fittings

This add-on covers accidental damage to fixed glass and sanitary fittings in your home.

Baggage

If your baggage is lost or damaged due to an accident or other incidents, you can add this coverage to your plan.

Electronic Equipment

You have the option to include coverage for your electronic devices, minimizing your financial liability in the event of damage.

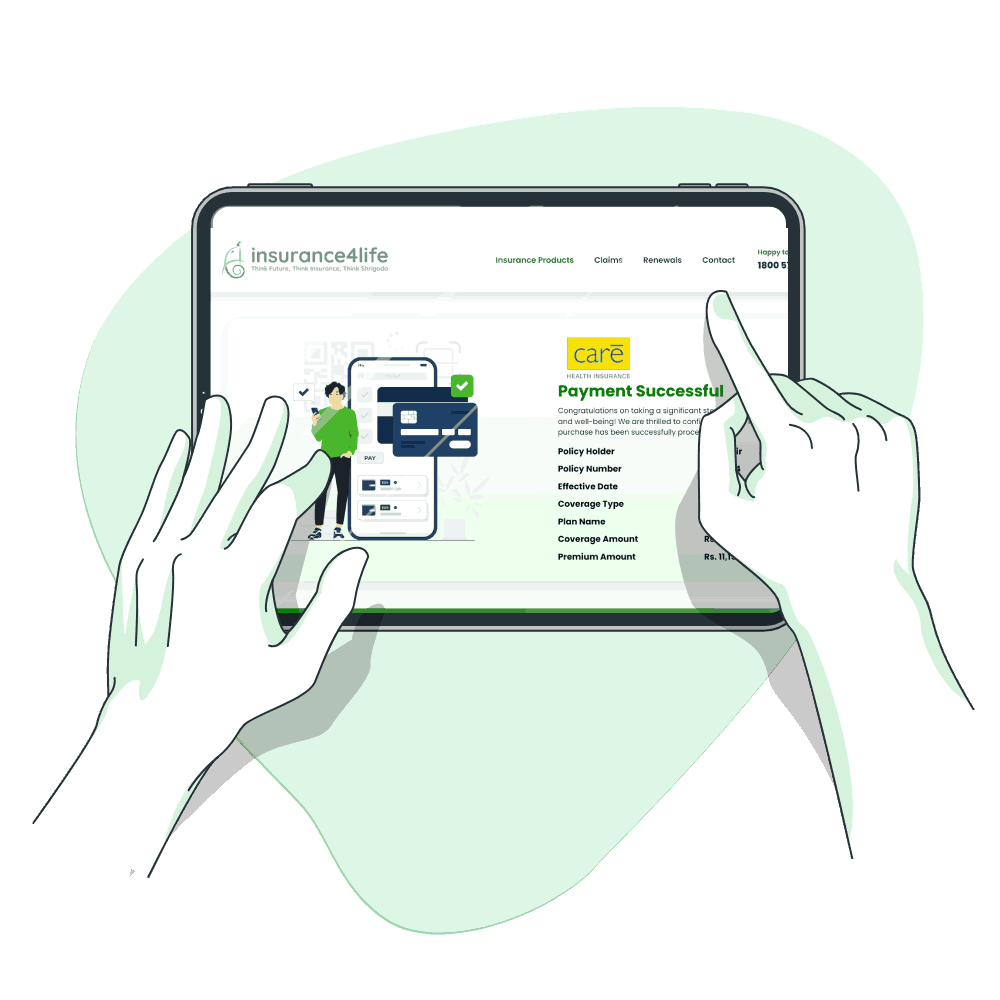

How To Buy Online Policy !

Get Quotes

Share your basic details like number of family members, their age and location

Choose plan

Select the ideal plan based on your needs and budget

Details Verified

Verification completed through secure online CKYC API

Payment Successful

Pay premium online & get your policy copy delivered instantly to your email inbox

Home Insurance FAQ:

Home insurance can cover the loss, damage, or theft of personal belongings, including furniture, electronics, jewelry, and clothing, both inside your home and sometimes outside (e.g., while traveling).

If your home is uninhabitable due to an insured event, home insurance can provide coverage for alternative accommodation (temporary housing) until your property is repaired.

Yes, many insurers offer flexible term options, allowing you to choose coverage from 1 to 5 years, eliminating the need for annual renewals.

Filing a claim usually involves contacting your insurer’s claims department, providing necessary documents (photos, receipts, police reports), and following their instructions. Many insurers also offer online claim submission for convenience.

Home insurance is not legally required in most places, but if you have a mortgage, your lender may require it to protect their investment.

Yes, many insurance policies allow you to add extra coverage for specific items or situations, such as high-value jewelry, home business coverage, or accidental damage. These are often called “add-ons” or “riders.”